LIFESTYLE

Health Insurance Unlimited Cover Reality: What Insurers Don’t Clearly Tell You About Medical Policies

Health insurance has become one of the most important financial protections for families today. Rising hospital expenses and costly treatments have pushed more people toward buying medical insurance plans. In recent years, insurance advertisements have aggressively promoted terms like “Unlimited Cover” and “Unlimited Restore Benefits,” making it appear as though policyholders will never have to worry about hospital bills again.

At first glance, the offer sounds extremely attractive. Many people assume that once they purchase such a policy, every medical expense will be fully covered regardless of the amount. However, insurance experts say the reality is far more complicated. The word “unlimited” often comes with several hidden conditions, restrictions, and fine-print clauses that many customers fail to notice while buying the policy.

Understanding these hidden details is extremely important before purchasing any health insurance plan.

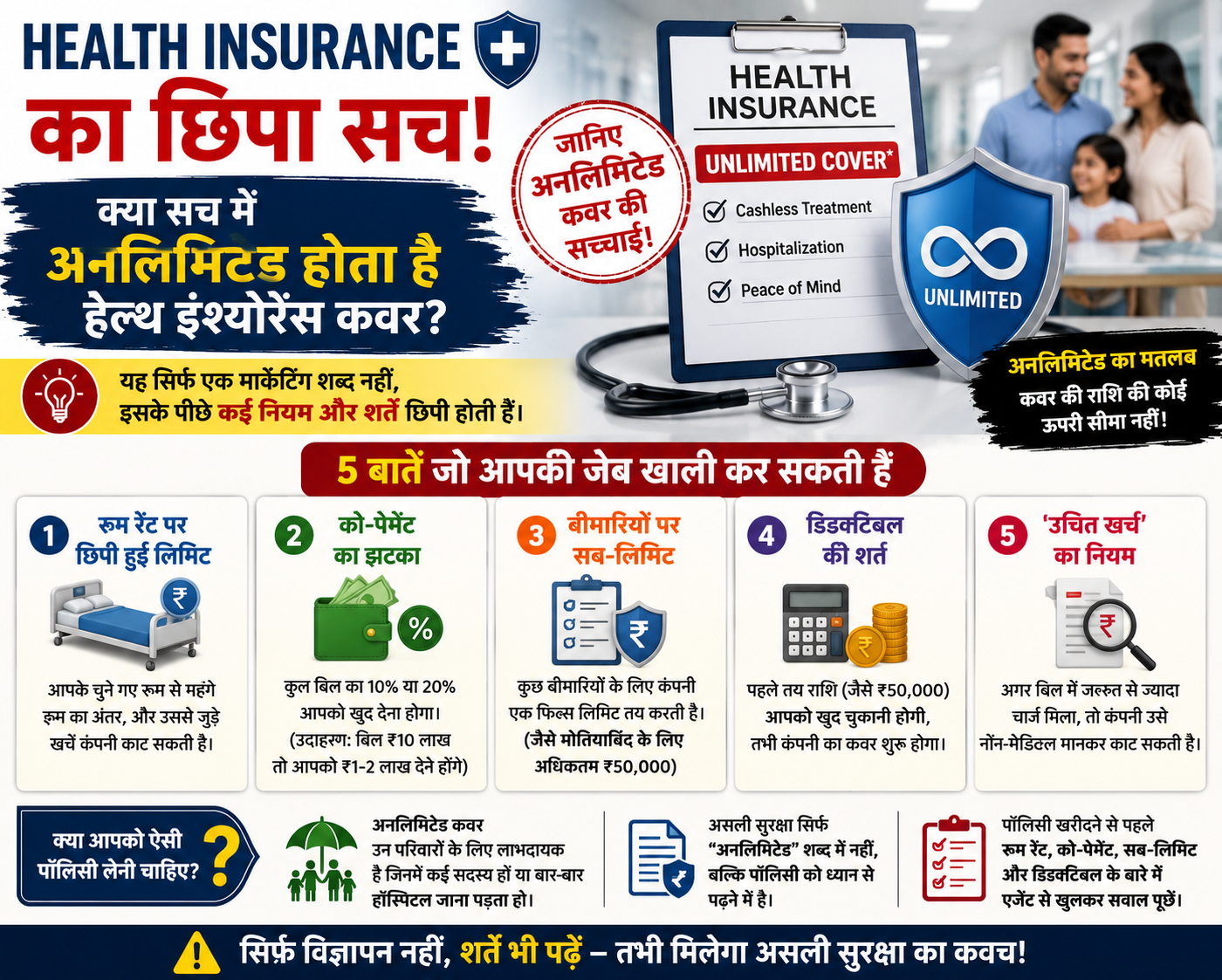

What Does ‘Unlimited Cover’ Actually Mean?

In most cases, unlimited cover does not mean that the insurer will pay every hospital bill without any limit. Instead, it usually refers to a restore or refill feature.

For example, if a person has a base health insurance cover of ₹10 lakh and that amount gets exhausted during treatment, the insurance company may restore the sum insured again for future hospitalization within the same policy year.

While this sounds beneficial, it does not guarantee that every medical expense will be paid in full. Several policy conditions can still increase the amount that customers must pay from their own pocket.

Hidden Conditions That Can Increase Your Expenses

1. Room Rent Restrictions

One of the most common hidden clauses in health insurance policies is the room rent limit.

Many insurers allow only a standard private room under the policy. If the patient chooses a more expensive room or luxury suite, the company may not only reduce the room rent reimbursement but may also proportionately cut other related expenses like doctor consultation charges, nursing fees, surgery costs, and hospital service charges.

As a result, policyholders may end up paying a surprisingly large amount despite having high insurance coverage.

2. Co-Payment Clauses

Another major condition is co-payment.

Under co-payment rules, the insured person must bear a fixed percentage of the total hospital bill. Depending on the policy, this can range from 10% to 20% or even higher.

For instance, if the hospital bill reaches ₹10 lakh and the policy has a 20% co-payment clause, the customer may still need to pay ₹2 lakh personally.

This is one of the biggest reasons why people often discover that their “unlimited” policy is not entirely cashless.

3. Disease-Specific Sub-Limits

Insurance companies also place sub-limits on specific treatments and surgeries.

Even if the overall policy cover runs into crores of rupees, common procedures such as cataract surgery, kidney stone treatment, hernia operations, or knee replacement may have fixed payout caps.

For example, a cataract surgery claim may be restricted to ₹50,000 even if the actual hospital expense is ₹80,000 or more.

The remaining amount must then be paid by the patient.

4. Deductible Conditions

Some modern insurance products include deductibles.

This means the policyholder must first pay a certain amount before the insurer begins covering the expenses.

If a policy has a deductible of ₹50,000, the customer must personally bear the first ₹50,000 of the medical bill. Only expenses beyond that amount will be covered by the insurance company.

People often overlook this condition while purchasing policies because it is not highlighted prominently in advertisements.

5. “Reasonable and Customary Charges” Rule

Insurance companies carefully examine hospital bills before approving claims.

If they believe that the hospital has charged excessively or that certain treatments were unnecessary, they may classify those expenses as non-medical or unreasonable charges.

These deductions can significantly reduce the final reimbursement amount.

Items such as gloves, registration charges, consumables, extra service charges, or premium room upgrades are sometimes only partially covered or completely excluded.

Should You Avoid Unlimited Health Plans?

Despite these limitations, unlimited restore benefits are not necessarily bad.

Such policies can be extremely useful for families where multiple members may require hospitalization during the same year. They can also help patients dealing with recurring illnesses or repeated treatments.

However, financial advisors recommend that customers should not buy a policy based only on marketing terms like “unlimited” or “100% coverage.”

Instead, they should carefully review:

- Room rent eligibility

- Co-payment conditions

- Waiting periods

- Disease-specific limits

- Deductibles

- Cashless hospital network

- Claim settlement ratio

- Exclusions and non-payable items

Why Reading the Fine Print Matters

Experts say many policyholders focus only on the premium amount and ignore the policy wording. This often leads to disappointment during emergencies.

Before purchasing any health insurance plan, customers should openly ask insurers or agents about all hidden conditions and written limitations.

A lower premium with strict restrictions may ultimately prove more expensive during hospitalization.

Smart Insurance Decisions Can Save Money Later

Health insurance remains an essential financial safety net, especially as medical inflation continues to rise in India. But true financial protection comes not from catchy marketing phrases, but from fully understanding the policy terms.

Choosing the right insurance plan requires comparing benefits, reading documents carefully, and understanding exactly what is covered and what is not.

In the end, the safest policy is not the one with the biggest advertisement, but the one that offers clear, transparent, and practical protection when it is needed the most.