BUSINESS

EPF Withdrawal Timing Explained: Should You Withdraw PF Before or After Interest Is Credited?

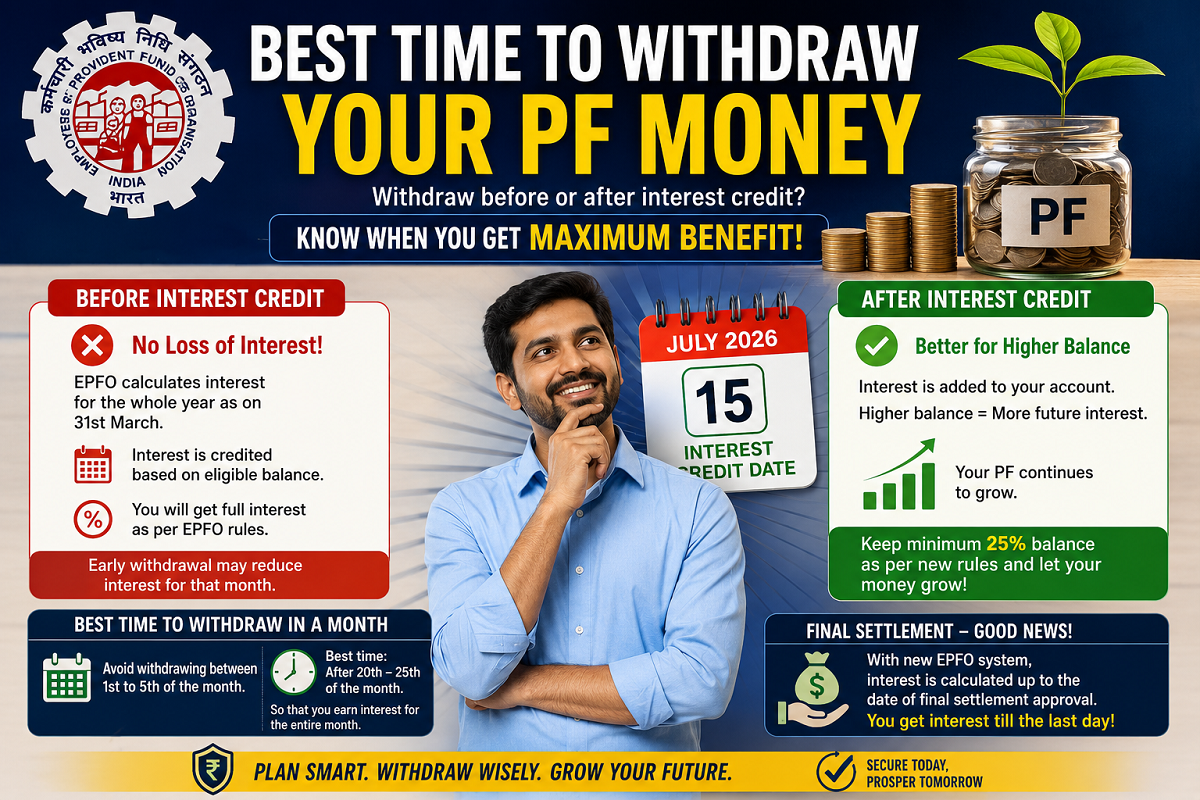

With the Employees' Provident Fund Organisation (EPFO) expected to begin crediting 8.25% annual interest for FY 2025–26, many subscribers are wondering whether they should withdraw their Provident Fund balance before the interest is reflected in their passbook or wait until after the credit is completed.

Understanding how EPF interest is calculated can help members avoid common misconceptions and make informed decisions when planning an advance withdrawal or final settlement.

Disclaimer: This article is intended for general information. EPF withdrawal eligibility and interest calculations are governed by EPFO rules and applicable regulations.

Does Withdrawing Before Interest Credit Result in a Loss?

One of the most common myths among EPF subscribers is that withdrawing money before the annual interest appears in the passbook means losing that year's interest.

According to EPFO's interest calculation process, this is not necessarily true.

Interest for each financial year is calculated based on the applicable balance and becomes payable after the financial year closes. Even if the interest entry appears later due to administrative processing or system updates, eligible members are entitled to the interest applicable under EPFO rules for the eligible period.

Therefore, the timing of the passbook update does not automatically determine whether interest is payable on an eligible balance.

Why Interest May Appear Later

Although annual interest is calculated after the close of the financial year, the credit may appear in members' passbooks later because of processing schedules and system updates.

This means that the visible credit date and the period for which interest is calculated are not always the same.

Members making eligible withdrawals generally receive interest in accordance with EPFO's applicable rules rather than the date on which the passbook is updated.

Best Time During the Month to Withdraw PF

Financial planners often suggest paying attention to the timing of a withdrawal within a month.

Since EPF interest is linked to monthly closing balances under the applicable calculation method, reducing the balance very early in a month could affect the amount that remains eligible for interest during that month's calculation period.

For this reason, members who have flexibility in their withdrawal timing may consider initiating the process later in the month rather than during the first few days.

While the exact financial impact depends on the withdrawal date and processing timeline, waiting until the latter part of the month may help preserve interest on the balance for that month.

New Rules Require Minimum Balance

Under the updated EPF withdrawal framework, eligible members making advance withdrawals are generally required to maintain a minimum balance of 25% of total accumulated contributions, subject to the applicable withdrawal category and scheme conditions.

Maintaining part of the retirement corpus allows the remaining balance to continue earning interest while preserving long-term retirement savings.

Instead of withdrawing the entire balance, members may find it beneficial to use advance withdrawal provisions only for genuine financial needs whenever possible.

Final Settlement Includes Eligible Interest

Members applying for final EPF settlement after meeting the prescribed eligibility conditions do not have to wait specifically for the annual interest credit date.

Under EPFO's upgraded centralized digital system, eligible interest is calculated according to the applicable rules up to the relevant settlement stage, ensuring that members receive the interest due as part of their final payment, subject to EPFO regulations.

This improvement is intended to simplify the settlement process and reduce delays for subscribers.

Points to Consider Before Withdrawing PF

Before submitting a withdrawal request, EPF members should keep the following factors in mind:

-

Understand whether an advance withdrawal or final settlement better suits your situation.

-

Check eligibility conditions for the specific withdrawal category.

-

If possible, avoid withdrawing the entire balance unless absolutely necessary.

-

Maintain the required minimum balance wherever applicable to continue earning interest on the remaining amount.

-

Verify that KYC details, bank account information, and UAN records are fully updated to avoid processing delays.

Plan Withdrawals Carefully

EPF is designed primarily as a long-term retirement savings instrument. While advance withdrawals are available for eligible needs such as medical treatment, education, marriage, or housing, members should plan withdrawals carefully to maximize long-term benefits.

Understanding how EPFO calculates interest and how withdrawal timing may affect account balances can help subscribers make more informed financial decisions while preserving retirement savings for the future.