Comparing Mutual Fund SIP and SSY Returns to Understand Which Option May Build a Larger Corpus for Your Daughter

Parents planning for their daughter's future often look for long-term investment options that can create a meaningful financial corpus. Two of the most popular choices are the Sukanya Samriddhi Yojana (SSY) and a Systematic Investment Plan (SIP) in mutual funds.

While both investments are designed for long-term wealth creation, they work very differently. SSY offers a government-backed savings scheme with an interest rate declared periodically, whereas SIP returns depend on the performance of financial markets.

If you invest ₹2,000 every month, which option could potentially generate a larger corpus? Here's a detailed comparison.

How Much Can a ₹2,000 Monthly SIP Grow?

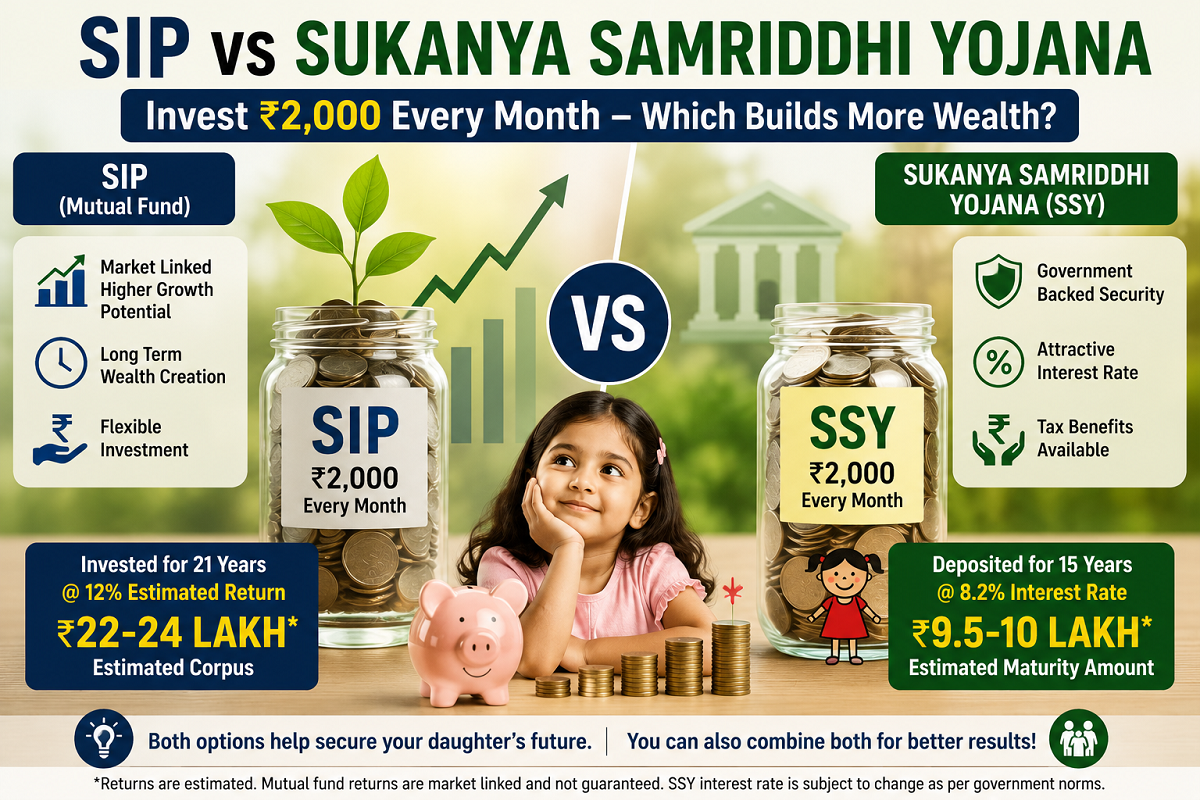

Assume your daughter is 2 years old, and you decide to invest ₹2,000 every month through a mutual fund SIP until she turns 23 years old.

If the investment earns an average annual return of 12%, the estimated outcome could look like this:

| Particulars | SIP Estimate |

|---|---|

| Monthly Investment | ₹2,000 |

| Investment Period | 21 Years |

| Total Investment | ₹5.04 lakh |

| Assumed Annual Return | 12% |

| Estimated Corpus | Around ₹22–24 lakh |

Although the total amount invested is only ₹5.04 lakh, the power of long-term compounding may help the investment grow to more than ₹22 lakh, depending on actual market performance.

It is important to remember that mutual fund returns are market-linked and are not guaranteed.

How Much Can Sukanya Samriddhi Yojana Generate?

Now consider the same monthly investment in the Sukanya Samriddhi Yojana, which currently offers an interest rate of 8.2% per annum (subject to periodic government revisions).

Under the scheme:

| Particulars | Sukanya Samriddhi Yojana |

|---|---|

| Monthly Investment | ₹2,000 |

| Deposit Period | 15 Years |

| Account Maturity | 21 Years |

| Total Investment | ₹3.60 lakh |

| Current Interest Rate | 8.2% per annum |

| Estimated Maturity Value* | Around ₹9.5–10 lakh |

*The maturity estimate is based on the prevailing interest rate. Future revisions in the government-declared rate may affect the final amount.

Unlike SIP, deposits in SSY are required only for 15 years, while the account continues earning interest until maturity after 21 years.

Why Is There Such a Big Difference?

At first glance, the SIP example appears to generate a much larger corpus.

However, the comparison reflects two different investment structures:

-

In the SIP illustration, investments continue for 21 years.

-

In SSY, contributions are made only for 15 years, after which the accumulated amount continues to earn interest without fresh deposits.

Another key difference is the assumed rate of return.

-

SIP illustration assumes an annual return of 12%.

-

SSY currently offers 8.2%, although the government reviews this rate periodically.

Because of these differences, the estimated maturity amounts vary significantly.

SIP vs SSY: Which One Should You Choose?

The right choice depends largely on your financial goals and risk tolerance.

Sukanya Samriddhi Yojana May Be Suitable If You Want:

-

Government-backed safety.

-

Stable returns.

-

Tax benefits available under applicable rules.

-

A dedicated savings plan for your daughter's future.

SIP May Be Suitable If You Want:

-

Higher long-term wealth creation potential.

-

Market-linked growth opportunities.

-

Flexibility to increase investments over time.

-

Better inflation-beating potential over long investment periods.

However, investors should remember that SIP returns are subject to market fluctuations and cannot be guaranteed.

Can You Invest in Both?

Many financial planners recommend combining both options instead of choosing only one.

For example:

-

₹1,000 per month in Sukanya Samriddhi Yojana.

-

₹1,000 per month in a diversified equity mutual fund SIP.

This strategy allows investors to benefit from the security of a government savings scheme while also participating in the long-term growth potential of equity markets.

As income increases over the years, investors may also consider gradually increasing their monthly contributions.

Final Takeaway

Both SIP and Sukanya Samriddhi Yojana are designed for long-term financial planning but serve different investment objectives.

SSY offers stability, government backing, and predictable interest, making it attractive for conservative investors. SIPs, on the other hand, have historically delivered higher long-term growth potential but involve market risk.

Before making any investment decision, individuals should assess their financial goals, investment horizon, and risk appetite. Consulting a qualified financial advisor can also help in selecting the most suitable investment strategy for a child's future.